INCOME PROTECTION

Ask the average Canadian what their most valuable asset is, and if you are a homeowner, you would likely say your principal residence. While that is likely true when it comes to something tangible you can buy or sell, it is far from your most valuable asset. Everything you own, activities you like, hobbies that interest you You and your ability to earn an income! What if you can’t earn an income?

DISABILITY INSURANCE

Your ability to earn an income is your most important asset.

What is the working life value of this indispensable asset?

This chart illustrates your total earning potential until age 65 based on your annual income and current age. When illustrated this way, you can grasp the significance of how valuable you are.

Your Earning Potential by age 65:

| Annual Income | At Age 25 | At Age 35 | At Age 45 |

| $35,000 | $2,359,089 | $1,536,595 | $894,063 |

| $50,000 | $3,370,128 | $2,195,135 | $1,277,233 |

| $65,000 | $4,381,166 | $2,853,676 | $1,660,403 |

| $90,000 | $6,066,230 | $3,951,243 | $2,299,019 |

| $120,000 | $8,088,306 | $5,268,324 | $3,065,359 |

| $150,000 | $10,110,383 | $6,585,405 | $3,831,699 |

Assumes an annual increase of 2.5%

Now, if due to a prolonged illness or injury you are unable to work, would it make sense to insure your ability to earn an income?

52% of Canadians do not have any coverage through an employer and of the 48% who have a group insurance plan, is that coverage enough to cover your monthly expenses?

CURIOUS?

Consider purchasing individually owned Disability Insurance:

Are you…

- Uncomfortable with the “definition” of disability of your group plan or the fact that your employer is the owner of the plan and can change or cancel it at any time?

- A business owner who relies on uninsured income sources like corporate profits and dividends?

- Have group coverage, however, are unable to insure the necessary amount of income due to plan limits?

- Your self-employed and your financial well-being is completely dependent upon you?

There are 3 options available depending on your situation:

- Purchase an individually owned plan that will cover the majority of your lost income (can be personal or business income)

- Purchase an individually owned plan as a top-up for the shortfall of your group coverage (the higher your income the more likely this scenario will come into play)

- Purchase an individually owned plan as an offset to your group coverage that can be relied upon should your group coverage end for any number of reasons (premium discounts available)

DID YOU KNOW?

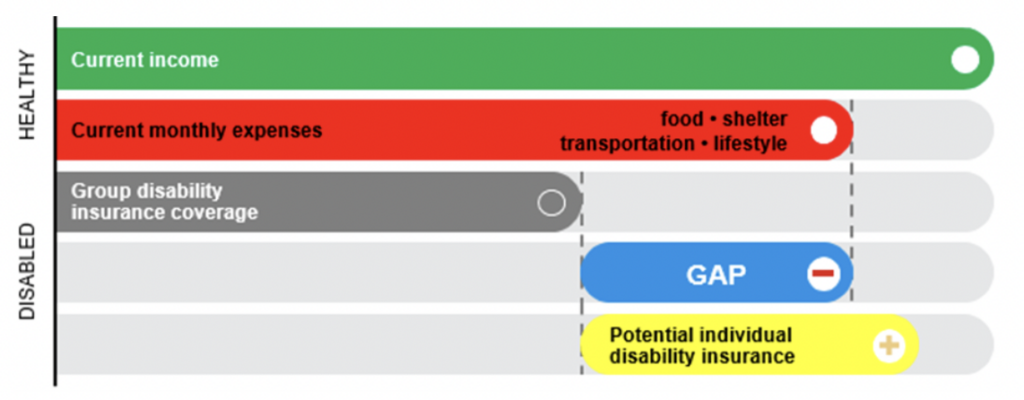

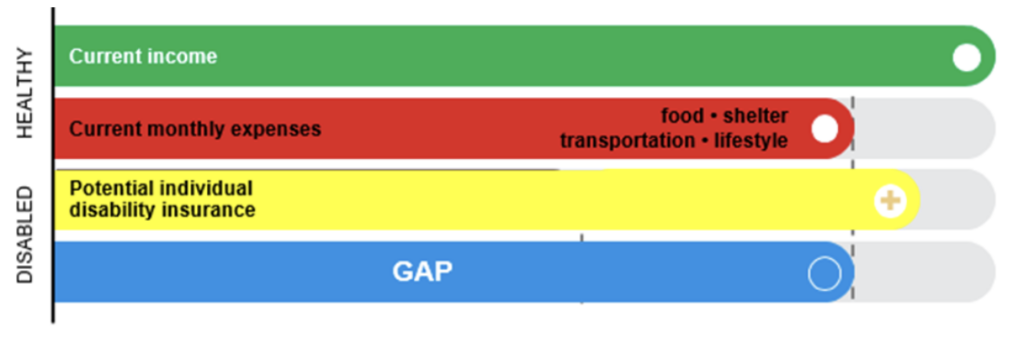

Group Top-Up Using Individually Owned Disability Insurance:

No Insurance or Group Offset:

Insuring the Full Amount Available Using Individually Owned Disability Insurance

The diagnosis of a Critical Illness frequently does not lead to a claim for Disability Insurance. Even though your “illness” may be disruptive and costly, you will not experience extended time off work. Yet you may encounter significant cost associated with your illness and your fight to return to good health. Not infrequently, survivors of serious illness do not want to resume their careers in the same way.

CRITICAL ILLNESS INSURANCE

…protects your assets so that this doesn’t have two costs associated with your illness…the toll on your body and the reduction in your hard earned assets.

What could be the impact upon your savings?

I'M CURIOUS

Protection from a major health event and a little forced savings for your healthy future self.

Critical Illness insurance provides you with tax free cash to be used as you want and in ways that give you options, both financial and physical. Home modifications; health care assistance provided by a nurse, therapist or similar professional; psychological counselling; These are just some of the costs that can be absorbed by Critical Illness Insurance. Money that might otherwise come from your savings. Further, one of the unique features in the Canadian living benefit insurance market is the ability to receive all your premiums back if you don’t claim on the contract.

DID YOU KNOW?

With Critical Illness Insurance you could get a cheque from the insurance company for every premium dollar you paid over the life of the contract. There is no other insurance product that allows you to receive all your premiums back if you don’t use it.

EXAMPLE

In the below example, during the 35 years of coverage, you are entitled to $100,000 tax free if you survive a major illness such as Cancer, Heart Attack, or Stroke for at least 30 days. There are many more covered conditions, however, these three are the most common that people will experience. Perhaps you know someone?

| Major Illness Recovery Benefit |

Female age 40 |

| Coverage to age 75 | $100,000 |

| Annual Premium | $1700/year |

| Total Premium returned @ age 75 |

$59,500 |

Imagine you received a check today for almost $60,000.

Now imagine your retired self receiving this cheque to supplement your retirement income.